At the same time, the US financial services sector will spend nearly $495 billion on technology in 2026, prioritizing cloud-native platforms and advanced software. This shift exposes a fundamental architectural mismatch: traditional MPLS-based WANs were designed to route traffic to private data centers, not distributed cloud services. Financial institutions managing thousands of physical locations need a network foundation that matches their digital transformation pace.

This guide covers what SD-WAN is, why it's particularly relevant for the financial sector, how it compares to legacy MPLS, what compliance implications it carries, and how to evaluate the right solution for your institution's specific requirements.

Key Takeaways

- SD-WAN replaces or augments costly MPLS circuits with software-managed routing across multiple connection types, giving financial institutions better performance, resilience, and lower costs.

- Key advantages: encrypted multi-branch connectivity, traffic prioritization for real-time transactions, automated failover, and 25–72% cost savings over MPLS-only architectures.

- SD-WAN supports PCI-DSS, GLBA, and FFIEC compliance through centralized policy enforcement, encrypted data flows, and detailed audit logging.

- Vendor-agnostic consulting ensures your SD-WAN architecture fits your compliance requirements, branch footprint, and cloud strategy — without locking you into a single vendor.

What Is SD-WAN and Why Does It Matter for Financial Institutions?

SD-WAN is a networking technology that decouples network control from the underlying hardware, allowing IT teams to manage and route traffic across broadband, LTE/5G, MPLS, and other links from a centralized software dashboard—rather than configuring each router individually. According to an IDC MarketScape analysis, SD-WAN provides automated management of hybrid WANs through "a centralized, application-based policy controller; a software overlay that abstracts underlying networks; analytics and/or telemetry for application and network visibility."

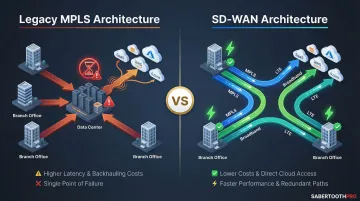

Most financial institutions operate dozens to hundreds of physical locations that all need secure, low-latency connectivity. JPMorgan Chase manages 4,881 branches, Bank of America operates 3,743, and Wells Fargo maintains 4,304 locations. Traditional hardware-based WAN architectures handle this complexity poorly — and at significant cost.

The shift to cloud-based financial applications amplifies these challenges. 60% of banks are moving at least 30% of critical workloads to the cloud by 2025, increasing bandwidth demand and making MPLS-only architectures a bottleneck.

Core banking platforms, payment processing, fraud detection tools, and CRM systems now run in distributed cloud environments rather than private data centers. That's exactly the traffic pattern MPLS wasn't designed to handle efficiently.

Dynamic Path Selection Changes Everything

Dynamic path selection continuously monitors all available connections and routes traffic over the best-performing link — with no manual intervention required. When a broadband circuit fails, failover to LTE backup happens in seconds with no dropped transactions. That automated resilience directly addresses the single point of failure that legacy single-link WAN architectures create.

SD-WAN is also the technical foundation that makes SASE (Secure Access Service Edge) deployments possible — a growing priority for financial services firms adopting zero-trust security models. SASE spending is forecast to reach $97 billion by 2030 as enterprises consolidate networking and security decisions into unified platforms.

Key Benefits of SD-WAN for Banks and Financial Services Firms

Improved Uptime and Business Continuity

SD-WAN's multi-link failover ensures that even when a primary circuit fails, transaction processing, ATM connectivity, and branch operations continue without interruption. This capability addresses the financial sector's most expensive operational risk: downtime.

The real impact:

- No single circuit failure disrupts customer-facing services

- Automatic rerouting happens faster than manual intervention

- Branch staff never experience network-related transaction delays

- ATM networks maintain continuous connectivity even during carrier outages

Lower WAN Costs Through Circuit Diversity

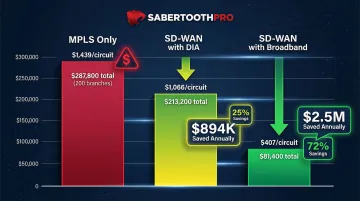

Financial institutions can replace expensive dedicated MPLS links with a combination of lower-cost broadband and 4G/5G backup circuits, managed intelligently by SD-WAN. According to Lightyear's 2026 cost analysis, a typical 1 Gbps North American MPLS circuit costs $1,439 monthly. SD-WAN using Dedicated Internet Access (DIA) circuits plus managed service costs $1,066 monthly—about 25% savings. Organizations using broadband-based SD-WAN typically save 50-84% on WAN costs.

These savings compound across large branch networks. A regional bank with 200 branches could reduce monthly WAN spending from $287,800 to $213,200 using DIA-based SD-WAN, or down to $81,400 with broadband circuits—creating annual savings between $894,000 and $2.5 million.

Application-Aware Quality of Service (QoS)

SD-WAN distinguishes between latency-sensitive traffic (real-time payment processing, VoIP for client calls, video conferencing) and lower-priority traffic (software updates, email), prioritizing the former automatically. Without this, a single busy branch internet circuit can degrade both VoIP call quality and card terminal response at the same time.

Practical application:

- Payment card terminals get guaranteed bandwidth during transaction processing

- Customer service VoIP calls maintain quality even during peak usage

- Branch manager video calls receive priority over background data syncs

- Cloud application performance improves without manual intervention

Centralized Visibility and Management

SD-WAN gives network teams a single dashboard showing traffic flows, link health, and anomalies across every branch. Instead of logging into dozens of individual routers, administrators manage the entire WAN from one centralized controller.

What this enables:

- Faster troubleshooting when branch performance issues arise

- Proactive capacity planning before congestion impacts customers

- Unified incident response across every location simultaneously

- Clear audit trails that support compliance reporting requirements

Scalability for Branch Openings, Mergers, and Acquisitions

Deploying SD-WAN at a new branch or acquired institution is far faster than provisioning traditional MPLS circuits. Zero-Touch Provisioning (ZTP) reduces deployment times from weeks to under 20 minutes per site, demonstrated by Investors Bank's recent rollout. MPLS circuits typically require 30 to 90 days to complete configurations and turn-up.

For banks growing through M&A, that gap is the difference between an acquired branch processing transactions on day one versus waiting three months for circuits to turn up. At 30-90 days per site, MPLS provisioning can stall integration timelines that executive teams and regulators are both watching closely.

SD-WAN Security and Regulatory Compliance in Financial Services

Financial institutions operate under a dense regulatory stack: PCI-DSS for payment card data, GLBA for customer financial privacy, FFIEC cybersecurity guidelines, and SOC 2 audit requirements.

SD-WAN's centralized policy management and encrypted tunnels help institutions enforce these requirements consistently across every location. Distributed hardware-based approaches leave room for configuration drift — exactly the kind of gap auditors flag during compliance reviews.

Built-In Security Features

Enterprise SD-WAN platforms include:

- End-to-end encryption (AES-256) for all traffic traversing the WAN

- Microsegmentation to isolate POS/ATM traffic from general branch traffic

- Integrated next-generation firewall capabilities managed centrally

- IDS/IPS functionality for threat detection and prevention

- Centralized security policy enforcement eliminating per-branch configuration variance

All security policies push from a central controller. That eliminates the per-branch configuration variance that auditors consistently flag during compliance reviews.

Regulatory Requirements Met by SD-WAN

| Regulation | Key Requirement | How SD-WAN Addresses It |

|---|---|---|

| PCI-DSS v4.0.1 | Strict change control + strong cryptography for data in transit | Centralized change management workflows + mandatory AES-256 encryption across all WAN links |

| GLBA Safeguards Rule | Report unauthorized acquisition of unencrypted customer data | Encryption ensures customer data in transit is never unencrypted, reducing breach notification obligations |

| FFIEC Guidelines | Network segmentation, encryption, and change management | Automated policy enforcement + detailed audit logs prevent configuration drift |

SD-WAN and SASE Convergence

Financial institutions increasingly pair SD-WAN with cloud-delivered security services — CASB, SWG, and ZTNA — under a SASE framework. This enforces zero-trust access for remote employees and contractor access to financial systems, both of which have expanded the attack surface in hybrid work environments.

The Forrester Wave finds that customers now prefer unified platforms from a single vendor to cut integration complexity and consolidate security services under one control plane.

SabertoothPro holds PCI-DSS and SOC 2 Type II certifications and draws on a 300+ partner ecosystem to recommend and deploy SD-WAN architectures built specifically for regulated financial environments.

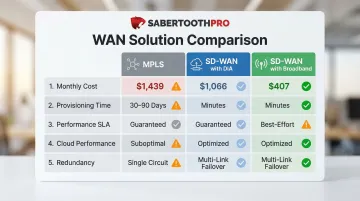

SD-WAN vs. MPLS: Choosing the Right Network Architecture

Financial institutions rarely face a strict either/or choice between SD-WAN and MPLS. Most deploy hybrid architectures that use both technologies where each performs best.

Direct Comparison

| Metric | MPLS | SD-WAN (DIA) | SD-WAN (Broadband) |

|---|---|---|---|

| 1 Gbps Monthly Cost (North America) | $1,439 | $1,066 | $407 |

| Provisioning Time | 30-90 days | Minutes to days (ZTP) | Minutes to days (ZTP) |

| Performance SLA | Guaranteed | Guaranteed (DIA underlay) | Best-effort |

| Geographic Flexibility | Limited by carrier footprint | Broad availability | Broadest availability |

| Cloud Application Performance | Suboptimal (hub routing) | Optimized (direct internet) | Optimized (direct internet) |

| Built-in Redundancy | Single circuit failure = outage | Multi-link automatic failover | Multi-link automatic failover |

Cost data from Lightyear 2026 analysis

The Hybrid Approach

SD-WAN doesn't require eliminating MPLS entirely. Many financial institutions keep critical inter-datacenter and trading-floor links on MPLS while shifting branch connectivity to lower-cost broadband managed by SD-WAN. The result: better resilience and real cost savings without a disruptive full cutover.

When MPLS alone is still appropriate:

- High-frequency trading environments requiring guaranteed microsecond latency

- Datacenter-to-datacenter replication with strict SLA requirements

- Markets where DIA costs as much or more than MPLS (some international markets)

When SD-WAN should be the primary architecture:

- Branch networks with 10+ locations

- Heavy cloud application usage (Office 365, Salesforce, cloud banking platforms)

- Geographic expansion into areas with limited MPLS availability

- Cost optimization initiatives with WAN spend reduction targets

How to Evaluate and Implement SD-WAN for Your Financial Institution

Key Evaluation Criteria

When selecting an SD-WAN vendor or solution, financial institutions should prioritize:

- Verify PCI-DSS, SOC 2, and ideally CMMC certifications before shortlisting any vendor

- Confirm AES-256 encryption and FIPS 140-2 compliance for data in transit

- Ensure the platform generates detailed audit logs that satisfy examiner requirements

- Check compatibility with existing firewalls, SIEM tools, and security stacks

- Validate MPLS + broadband + LTE management within a single architecture

- Request references from financial institutions of comparable size and complexity

Practical Implementation Approach

Phase 1: Network Audit

- Document existing circuits, costs, and contract terms

- Profile branch traffic patterns and application dependencies

- Identify latency-sensitive applications requiring QoS prioritization

Phase 2: Pilot Deployment

- Select two or three representative branches for initial deployment

- Define QoS policies and security segmentation rules before go-live

- Configure monitoring dashboards to provide compliance audit visibility

Phase 3: Phased Rollout

- Deploy to additional branches in waves (typically 10-20 sites per wave)

- Monitor performance metrics and adjust policies based on real usage

- Document configuration standards for consistency across all locations

Phase 4: Ongoing Management

- Establish regular performance review cycles

- Update security policies as new threats emerge

- Plan capacity upgrades based on dashboard analytics

The Vendor-Agnostic Advantage

Getting through a multi-phase rollout is one challenge — choosing the right platform architecture upfront is another. That vendor decision shapes every phase that follows.

Working with a vendor-agnostic technology advisor like SabertoothPro changes that calculus. Their 300+ partner ecosystem lets them benchmark solutions against your specific compliance requirements, traffic profile, and budget — not the other way around. Their national installer network also coordinates field deployment across multiple branch locations, removing the friction of managing separate installation vendors site by site.

The practical result: your institution lands on the SD-WAN platform that fits how you actually operate, not the one a single vendor is incentivized to sell.

Frequently Asked Questions

Is UCaaS worth the investment for financial institutions?

Yes. UCaaS replaces fragmented legacy phone systems with a unified, cloud-based platform that supports compliance-ready call recording, lower operational costs, and faster customer response. SD-WAN typically serves as the network foundation that keeps UCaaS performing reliably across branch locations.

What is the difference between SD-WAN and MPLS for banks?

MPLS is a dedicated, private circuit that offers guaranteed performance but high cost and slow provisioning, while SD-WAN uses software intelligence to route traffic dynamically across multiple lower-cost connections. SD-WAN gives banks comparable reliability at substantially lower WAN spend, especially across large branch networks.

Does SD-WAN meet PCI-DSS compliance requirements?

SD-WAN can support PCI-DSS compliance through end-to-end encryption, network segmentation of cardholder data environments, and centralized policy enforcement. However, compliance depends on proper configuration and the security capabilities of the specific SD-WAN solution chosen—not all platforms offer the same security features.

How does SD-WAN support business continuity for financial institutions?

SD-WAN's automatic failover across multiple WAN links (broadband, LTE, MPLS) ensures that branch operations, ATM connectivity, and payment processing continue uninterrupted even when a primary circuit fails. Legacy single-link WAN architectures offer no such redundancy—one outage takes down the entire branch.

How long does it take to deploy SD-WAN across a multi-branch bank?

Zero-touch provisioning can cut individual branch deployment from weeks (standard for MPLS) down to hours. That said, enterprise rollouts spanning dozens or hundreds of locations are typically phased over several months to allow for proper testing and staff training.